The models of Thomas Lux (1997, 1998, Lux & Marchesi, 1999,

2000) are multi-agent (without individual agents !) simulations of financial

markets. Lux purpose is to replicate the statistic stylized facts observed in

real markets, namely :

- Fat tails (series are leptokurtic)

- Volatility clustering (large fluctuations are followed by large

fluctuations) and even...

- The hyperbolic decay of the volatility autocorrelation ( the

so-called long memory property).

These features of financial data imply that the probability distribution

function is highly non-gaussian. This simulation shows that with gaussian

information arrivals, and a market composed of heterogeneous agents who switch

between different strategies, the price exhibits the characteristics of real

data.

The Model

This kind of model is used by an increasing number of authors, see, e.g.

Youssefmir and Huberman [1997] and Kirman [1993] among others. In a complex

environment, adaptive agents continuously switch between different strategies,

influenced in their decisions by the interactions with other investors. The

population of investors is divided into two groups, chartists (using past

data to infer future price) and fundamentalists (they trade only on

information). The chartist group is also divided in two sub-groups, the "optimistics",

who extrapolate the price trend (positive feedback trading) and the "pessimistics"

who believe that the price will revert (negative feedback trading, the so-called

"contrarian" strategy). In this setting, agents compare profits

obtained with these different strategies. As the chartist profits depends on a

opinion index, mimetism is introduced. This leads to large waves of optimism and

pessimism. Readers may refer to the different articles of Lux to understand the

transition probabilities between different strategies of trading.

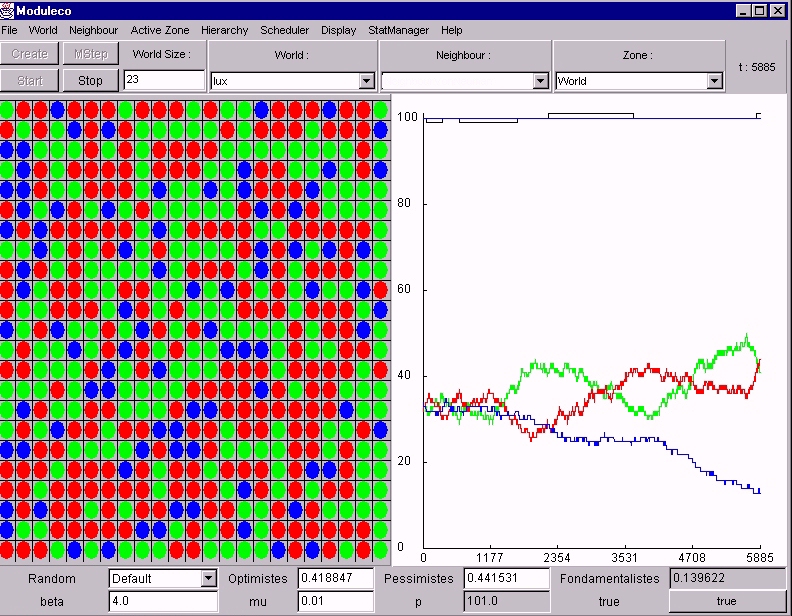

Note : in Moduleco, the right-part graph represents the

evolution of the market price (which is arbitrarily fixed to 100 at the

beginning, and is equal to the fundamental price) and the fractions of different

groups, namely, blue for fundamentalists, green for optimistics and red for

pessimistics.

note writing by Nicolas

Boitout, Sebastien Chivoret, Thierry

Delahaut

- Kirman A. [1993], ' Ants, rationality and recruitment', Quarterly

Journal of Economics, Volume 108

- Lux T. [1997], 'The socio-economic dynamics of speculative markets:

interacting agents, chaos, and the fat tails of return distributions, Journal

of Economic Behavior & Organization, Volume 33

- Lux. T [1998], 'Time variation of second moments from a noise

trader/infection model, Journal of Economic Dynamics and Control,

Volume 22, Issue 1

- Lux T., M. Marchesi [1999], 'Scaling and criticality in a

stochastic multi-agent model of financial market', Nature vol. 397 pp

498 - 500

- Lux T., M. Marchesi [2000], 'Volatility clustering in financial

markets: a microsimulation of interacting agents, International Journal

of Theoretical and Applied Finance

- Youssefmir M., B. A. Huberman [1997],'Clustered volatility in

multiagent dynamics', Journal of Economic Behavior & Organization,

Volume 32, Issue 1

Denis.Phan@enst-bretagne.fr

; Antoine

Beugnard@enst-bretagne.fr